Reshaping card issuers in the face of digital disruption

Businesses are shifting to more inventive and robust systems offerings as credit card issuers face increased pressure from digital disrupters.

In summary:

- Conventional credit card issuers, whose ability to respond is hampered by delayed, expensive legacy systems - are currently witnessing their revenues squeezed by digital competitors.

- QR codes, POS financing, card aggregation platforms, and e-commerce offerings present the critical need for card issuers to reshape.

- Companies are reacting by enhancing more value-added customer offerings, revamping platforms, and utilizing innovative fraud-fighting tools.

The COVID-19 pandemic has speeded up the rise of digital payment methods such as contactless and card-not-present transactions, prompting card issuers to transform rapidly. Companies that consider adapting through differentiated products and services can boost robustness and competitive edges in a volatile market.

Three pain points put credit cards aunder tension.

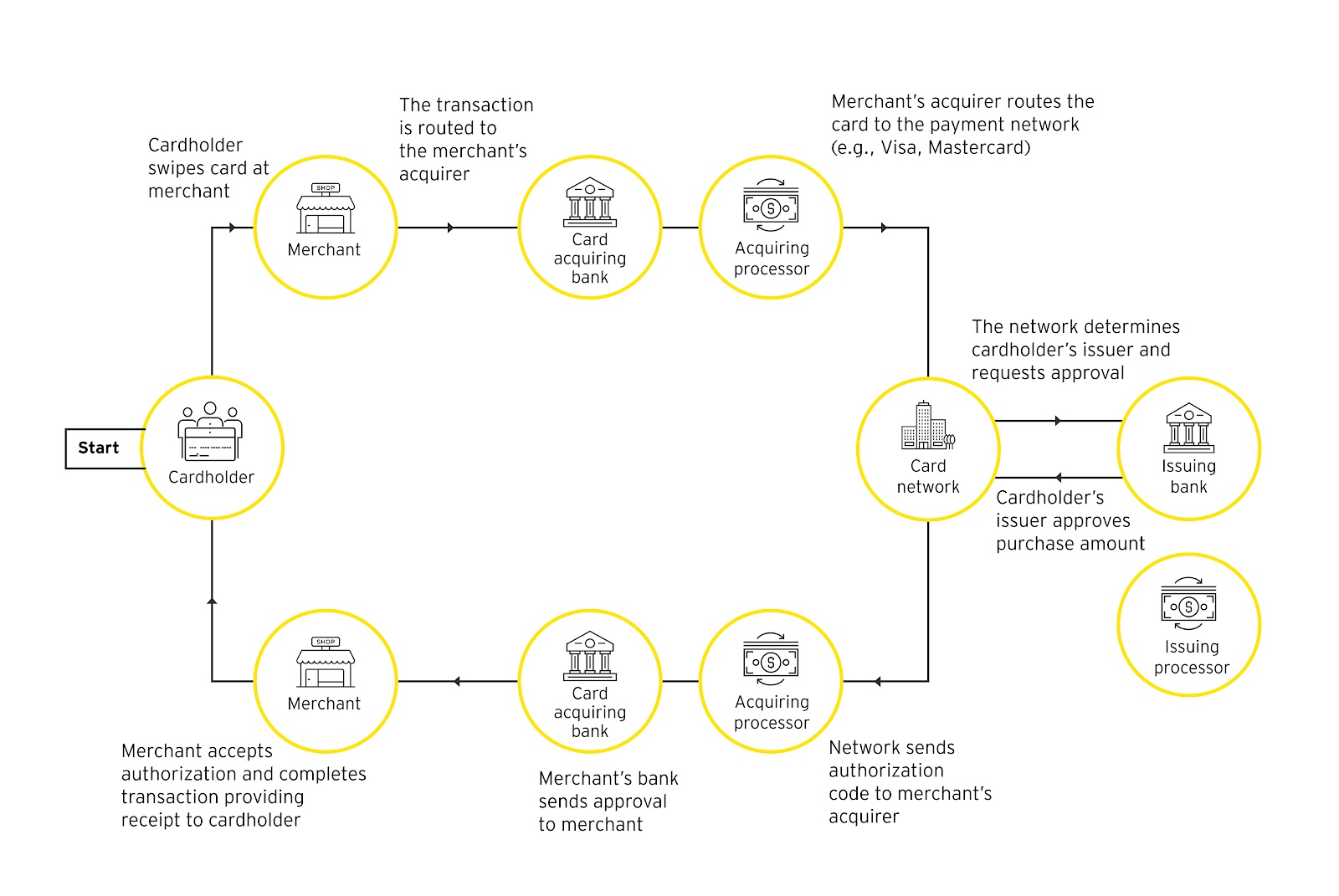

In 2020, the traditional card life cycle facilitated US$6.75 trillion in personal and commercial spending. This life cycle could include the origination and adjudication, clearing, settlement, fraud, customer service, and collections services, subjecting the issuing bank.

Conventional card transaction life cycle:

Card issuers, on the other hand, are losing influence to digital competitors, with three pain points putting traditional approaches under pressure:

- Slow in adapting

Legacy systems that are difficult to configure impede card issuers' ability to make dynamic changes to card offerings, reducing competitive advantage.

- High operating expenses

Running legacy systems can be costly, as they necessarily require specialized resources to develop and test changes as well as run mainframe legacy applications such as COBOL.

- High replacement cost

Changing providers and establishing a new processing platform can be time-consuming and disruptive. A large issuer's core credit card processor can interface with over 100 upstream and downstream enterprise applications.

How is the credit card industry adapting to the arrival of digital newcomers?

As card issuers face these challenges, new competitors are gaining market share, with four key disruptors to the traditional model:

Traditional card transaction life cycle disruptors:

1. QR codes

QR codes satisfy customers’ needs for contactless payments while also offering merchants the potential of lower acceptance costs if the transaction is facilitated by an Automated Clearing House (ACH) rail.

Legacy card networks are responding by diversifying product portfolios through acquisitions and new products, to maintain as much transaction volume as possible.

2. Buy-now-pay-later at the point of sale

Among several fastest-growing consumer lending products, POS financing is predicted to grow at an average annual growth rate of 28 percent through 2023.2

Its potential to maximize sales appears as a great incentive to merchants, while the deferred payment options offered by POS are highly appealing to customers. However, the popularity of POS is hurting transaction volume and interchange for card processors, issuers, and networks. Many people are fighting back by banding together to offer similar solutions.

3. Card aggregation platforms

Card aggregation platforms enable consumers to choose which card to use for a transaction after the point of sale, giving them time to evaluate incentive offers. While these platforms have little to no impact on interchange or transaction volume for processors or issuers, they do stress the importance of providing enhanced rewards and incentives to market faster in order to remain competitive.

4. E-commerce offerings for access by the unbanked and underbanked population

Approximately seven million US households did not have a bank account as recently as 2019, thus reducing their opportunity to purchase online.3 Given this discomfort, a number of e-commerce leaders have introduced new payment solutions for these customers, allowing them to pay with cash, wallets, and bank transfers, and complete transactions at local stores.

While these e-commerce offerings do not necessarily affect traditional card players' revenue, business owners should consider how to remain competitive in this fast-growing market with huge potential for growth.

How are payment players reacting?

Card issuers are reacting to increased competition and innovation by developing advanced, adaptable platforms that enable them to develop and commercialize the feature-rich choices that customers desire rapidly.

1. Enhancing customer-facing products

Card issuers are improving the consumer experience with new features such as enhanced incentives and personalization, and they are adapting rapidly when situations change. For instance, COVID-19 saw an increase in demand for virtual cards, a trend that is likely to continue. JP Morgan has partnered with Marqeta to provide virtual issuance to commercial cardholders, who can then spend instantaneously via mobile-wallet provisioned cards.

Another trend driven by the epidemic and set to continue is more dynamic incentives and perks. Some issuers have allowed clients to convert premium travel perks to home-used advantages, while others have eliminated yearly payments for individuals who are under stress. Issuers are also providing advantages that appeal to consumers' interests, such as assistance for small companies and environmental sustainability. Several debit cards on the market now offer bitcoin incentives. This capacity to distinguish will be crucial in defeating emerging payment solutions that endanger card transaction income.

2. Modernizing card platforms

Customers' expectations in financial services have risen as a result of the simple and intuitive experiences provided by top online merchants and digital platforms. To stay updated, card issuers must implement microservice-based technological designs, increasing usage of application programming interfaces (APIs), and cloud-based processing infrastructure hosting.

Microservices architecture organizes an application as a set of services structured around business processes and applicable independently. This enhances flexibility by permitting component-level updates without interrupting larger systems. Microservices design also provides for the selection of the programming language better suited to the purpose of that element, allowing for the critical speed to market required to retain an issuer's competitive edge.

APIs also boost competitiveness by allowing the intersystem connection needed to provide customers with the omnichannel experiences they expect. Different APIs meet different demands, and card issuers must evaluate their size, services, and priorities when deciding how to proceed.

When compared to conventional processors, cloud-based hosting produces greater adaptability, productivity, and cost reductions. Regular manufacturers are developing to keep up with cloud-based solutions such as those from Marqeta. Global Payments, for example, has announced a collaboration with Amazon Web Services (AWS) to develop an industry-leading, cloud-based issuer processing platform. Cloud-based processors deliver scalability and enhanced security, as well as the advantage of low cost on infrastructure management.

3. Digital tools to enhance credit card fraud management

Fraud still arrives as a major concern for card issuers and processors. Payment card fraud losses totaled US$28.65 billion in 2017, with the pandemic bolstering huge rise in fraud activity. Fraud continues to be a focus for card issuers and processors. Payment card fraud losses totaled US$28.65B globally in 2019, with COVID-19 further fuelling significant growth in fraud activity.

Synthetic fraud is among the most prevalent kinds of credit card fraud, in which phony personally-identifying information (PII) is used to build new credit profiles. Fraudsters can keep these profiles up to five years, leaving it exceedingly difficult to uncover bogus accounts. Card companies are combating the activity with more sophisticated data mining tools that can distinguish between actual and fraudulent profiles. For example, Visa's Advanced Identity Score generates a risk score for new account applicants using artificial intelligence and machine learning capabilities. The idea is that actual individuals leave data traces that may be tracked for years after PII is removed, while synthetically created consumers do not exist prior to the establishment of their credit profile. We anticipate that these abilities will acquire momentum as measures against larger fraud across the sector.

How to determine the best path forward for transformation?

Organizations should first define their ultimate objective before determining which innovations will be included in their development. Is the ambition to be the first to market or to deliver the most creative items that drive change? To boost resilience in the face of adversity? To improve client-centricity or digital savvy?

The route forward for various card issuers will vary, just as the purpose driving change will vary greatly depending on a company's client base, geography, and future aspirations. To remain competitive in a rapidly changing market, everyone will need to adapt to the primary trends altering their field. Issuers must evaluate how they will diversify their revenue sources, leverage on future technology, and maximize existing services by questioning themselves:

- What items and services do our consumers desire and expect?

Understanding consumer expectations could significantly foster the creation of innovative products. Utilizing sophisticated analytics can assist businesses in forecasting the demands of potential future consumer groups.

- How can we provide in a way that fulfills the needs of our customers? Competitive advantage will be determined by the capacity to sell advanced offerings to the largest growing client categories.

- Can we make FinTech collaborations happen for us? Companies should consider if it is more effective to develop, purchase, or cooperate to meet their needs. A card issuer is considering working with a FinTech agent to tackle a specific use case. A firm that wants to address numerous issues, such as scalability, flexibility, and speed to market, may benefit more from investing in an end-to-end card issuing platform conversion.

- Where do our perseverance gaps exist? To increase robustness, businesses may need to enhance current platforms and/or establish new ones.

Answering these questions may serve as a basis for card reformation strategic planning at any scale, ensuring that outcomes meet an issuer's key growth drivers and overall card strategy.

References

- “U.S. General Purpose Brands,” Nilson Report website, February 2021.

- “The Rising Popularity of Buy Now, Pay Later (BNPL),” PYMNTS.com website,6 April 2020.

- “How America Banks: Household Use of Banking and Financial Services: 2019 FDIC Survey,” Federal Deposit Insurance Corporation website, October 2020.

Source: ey.com