What the hell is a neobank?

What neobank did to stir up the financial markets, even the elder brother of traditional banks was also affected. The growth of neobank has given customers new options for banks to worry about. Whether they really are better or just the fun created by the big guys.

What is a neobank, neobank definition signs of their future development and the most complete view of neobanks in Australia? All will be clearly shown below. Don't ignore it as you may confuse neobank with that challenger bank.

What a neobank is not

Perhaps it would be easier to start with “What a neobank is not” questions.

First of all, it's not just a digital bank, it's the same as neobank vs digital bank

Of course, most of the banks have already built mobile apps. And the era of online banking started to explode from here. But it is not enough to inherit and develop the digital system of the 4.0 era. ING, UBank, ME Bank - famous digital banks, but they are not neobanks. Simply put, because they only have a simple digital platform, they connect with an established organization, taking advantage of the existing infrastructure.

And neobanks are not simply challenging banks, they have more than that.

Neobank is a misconception because challenge bank is not defined as digital banking or neobank but it only poses challenges for large traditional banking. All new banks are challenge banks, but not all challenging banks are new banks ...

Neobank is not brick and banks are mortar.

You can not sit in line to wait, wait and talk to tellers through the glass screen. They provide all the digital experiences, the right user experience apps for target customers.

So, what is a neobank

Today, when technology 4.0 is strongly applied to life, many new applications are born. They are packed with better features and are more user-friendly. And in which there is the appearance of a digital bank that is known as neobank. So what is a neo-banking, and how is it changing the financial scenario?

Neobank meaning is a virtual bank, without any branches built up. The operations of this bank are completely online instead of going to the transaction points. neobank provides its customers with an experience through a Mobile Application (App) that should be called digital banking.

Neobanks have changed the context of the finance and banking industry when now you do not need to remember customers, without meeting with customers, you can still generate revenue and help a lot for customers. With the main purpose of providing a seamless customer experience, these new banks offer a wide range of outstanding features, the best solutions that traditional banks cannot. Faster, cheaper cost, smoother processing, and especially all platforms are integrated into one Mobile App.

What is neobank?

Read this article again to avoid confusion and answer the question "What is a neobank?".

See more: https://finfan.vn/News/what-is-a-neobank-401

Neobank - 1 Multi-Experience Application

- Open an account

- Payment and money transfer at home and abroad

- Home Loan

- Other services such as Investment, Expenditure management,...

Every day, thousands of Mobile Applications are opened, providing more digital utilities, more optimized solutions. And the integration of banking technology and services in one application is also inevitable. Increasing demand has forced digital banks to change themselves for the better, more active and friendly.

At the same time, the AI platform, chatbox can analyze customer samples, credit history, finance, and many different data to suggest necessary information to customers.

In a way, neobank is offering multitasking that cannot be done by traditional banks. From simple things like making payments, transferring money domestically, to difficult things like remittances, transferring and receiving money from abroad are now extremely simple.

All about the benefits of digital payments solution

Vietnam has never forgotten how traditional banks have helped improve the financial sector. However, the change at this time is extremely necessary because of the positive changes brought by neobank.

How neobank is doing

The neobank business model is different from traditional banks from engineering to operation compared. The business model that this new bank is based on technology platforms like AI (artificial intelligence) or Blockchain, Big Data. Do not use a cumbersome HR operator, no branch transaction, but all are integrated on a Smart Mobile Application platform.

As noted above, neo-banks are moving toward personalized services, with a priority on convenience. Because all neobank's problems are handled digitally, and technology plays an important role in the operating model here. Most neobanks rely on data sources analyzed from customer behavior to make decisions and operate for it. They collect and analyze data through the user's actions and the user's final decision.

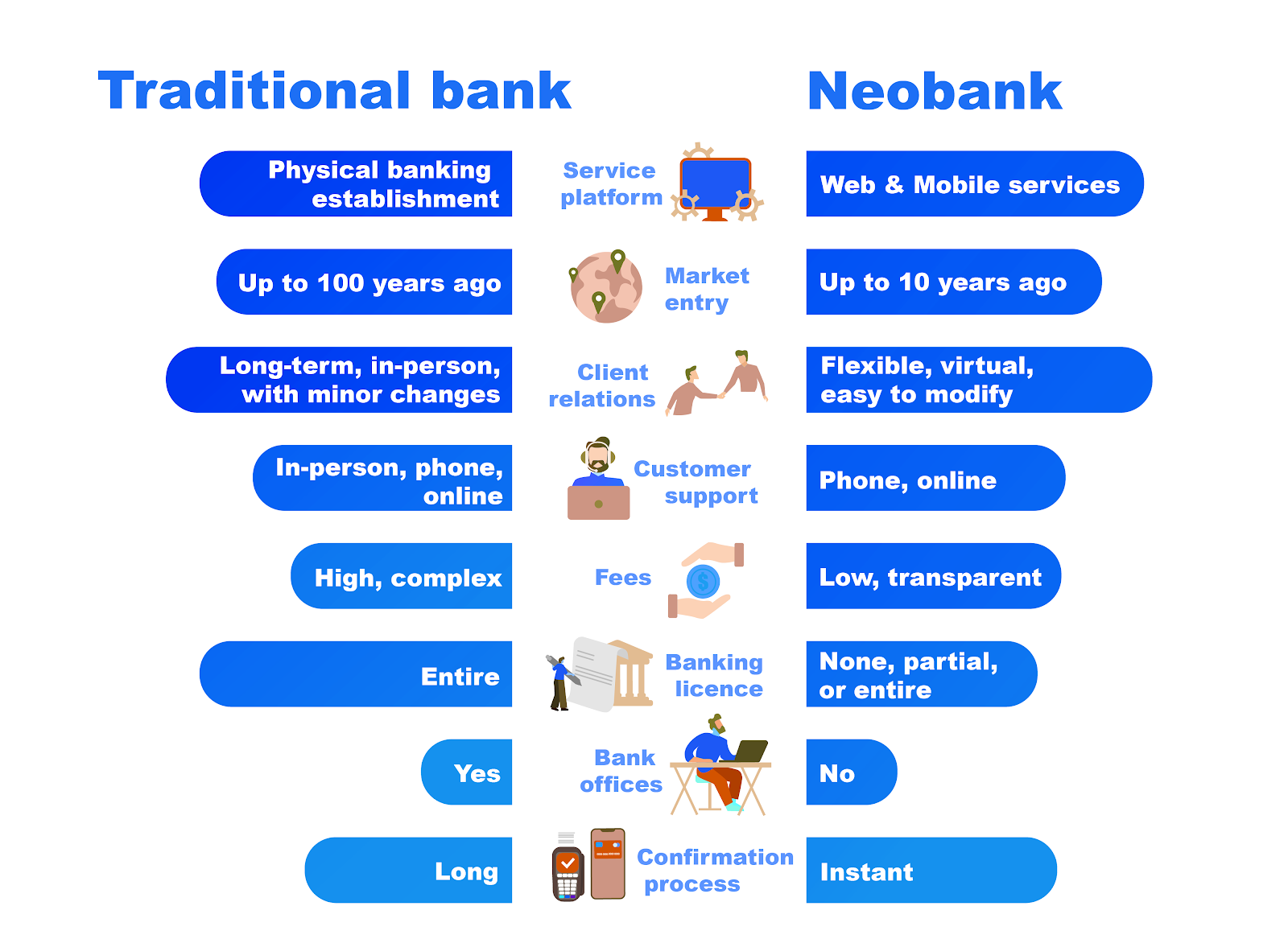

The big difference between neobank and traditional bank

Basically, neobank fintech differs from traditional banking in every aspect from the business model to operation and customer care.

As mentioned above, traditional banks have platforms that provide customer service from the point of sale, while the new bank is entirely using a mobile application to take care of customers (no transaction point). Traditional banks need more space costs (ongoing costs of rent, electricity, security, etc.) and they are required to collect from customers in the form of transactions such as bank statements, notices bank, money transfer or card,.. to pay those expenses.

While the neobanks have few costs and are accounted for transparently. Neobanks with or without some or all of banking licenses. But for traditional banks, the state requires licenses to be complete and thoroughly vetted.

Traditional bank vs neobank

Any approval process (opening an account, transferring and receiving money, etc.) for physical banking takes many stages as it is a multi-level process. The top neobanks make many of these lengthy tasks more automatic and quick.

Neobank’s customer care also relies on a combination of self-chat-capable bots and AI that provide flexible, virtual, online support while traditional banks rely on private telephone and consultant for customer support. Using people to take care is much more friendly than using a bot, but this also brings a lot of trouble for mainstream banks.

How neobanks make money?

Since neobanks have lower overheads than traditional banks, they can increase their profit margins. If they partner with banks instead of getting a charter, this can result in lower fees, with costs remaining even lower.

Other ways of getting money from neobanks include paying for ancillary services, charging interest on deposits, providing credit (although not necessarily to consumers) and charging businesses through credit or debit card transactions.

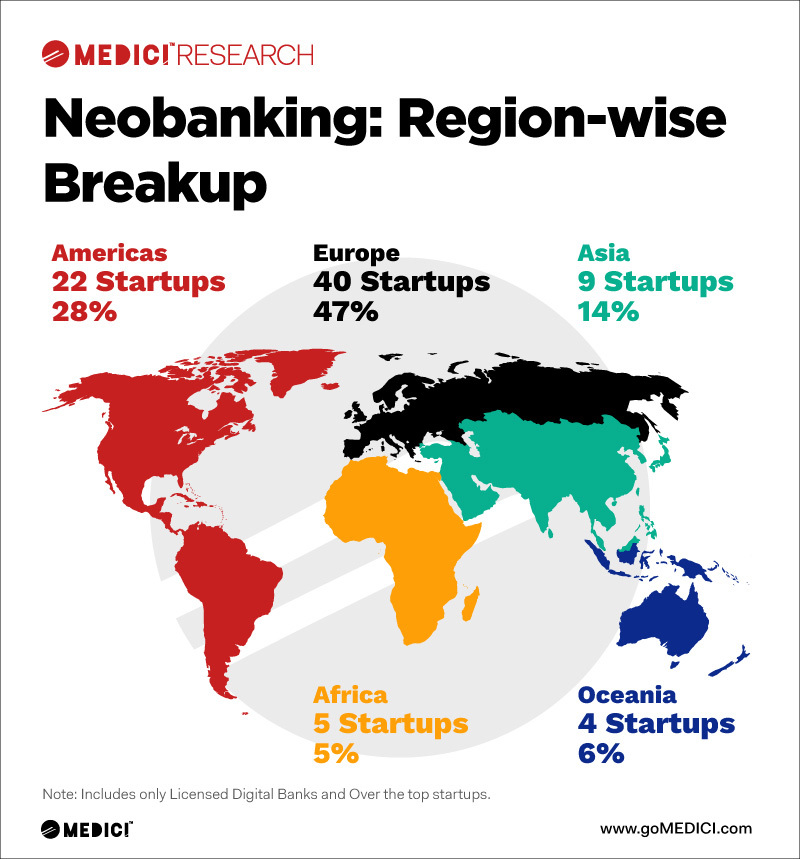

Types and examples of neobanks

Although initially, they may seem very similar to each other in terms of how they manage transactions, there are crucial differences that depend on their licensing system.

In this section, we present the most common types of neobanks with examples of each.

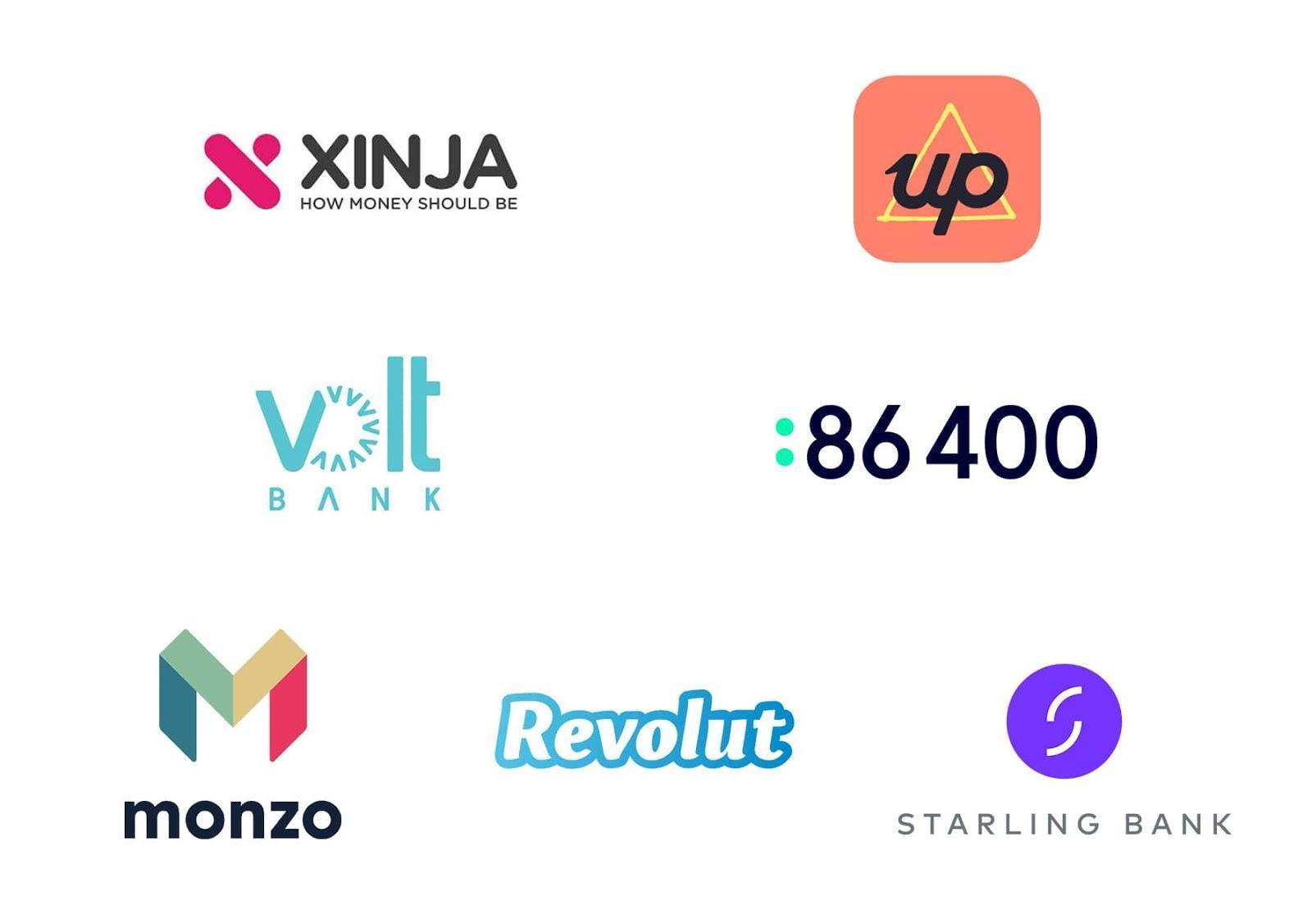

- With their own banking license: Most popular neobanks operate with their own banking license, either specialized or full range. With the right license, they can provide their own checking accounts, prepaid, debit or credit cards, currency exchanges, crypto-currencies, money transfers, retail payments, savings accounts and loans.

Examples: bnc10, N26, Revolut, Monzo, Starling Bank, Atom Bank.

- Without banking license: Neobanks that offer financial services, but with licenses from other banks. Customers may already have an account at another bank, which is linked to the neobank service that provides its own unique interface and tools for their bank account operations. The tools could be transaction analysis, budget management and automated notifications to help users achieve their financial goals. Other neobanks also use the license of a partner bank (parent company) to offer their financial products.

Examples: Yolt, Simple, Chime Bank.

- Beta Banks: Financial services subsidiaries of a larger and more consolidated bank that wants to reach more customers or develop new products under a different brand. Beta banks can offer their offerings under the license of the parent bank and expand to other countries through the licenses of the partner banks. Services can be limited initially and expanded as they gain popularity.

Example: B next, Mettle, Sberbank Direct.

World’s Leading Neobanks

The following are among the largest neobanks:

- Chime (US), a mobile bank with no hidden fees on Visa debit cards and debit and savings accounts, is currently valued at US$14.5 billion.

- Varo (US) is the third-largest neo-bank in the US as of 2020, behind only Courant and Simply. It is the first neo-bank to be granted a national banking license (separate license).

- Dave (USA), a billion-dollar start-up, has joined the elite Unicorn Club. Its mission is to help solve pressing financial problems: closing the payment gap without additional bank charges, getting interest-free loans, finding temporary work and improving credit ratings.

- Monzo (UK) is one of the first IT start-ups in Europe and one of the few with a banking license, which is only available under UK and Australian law.

- Revolut (UK) is ranked second in terms of capitalisation at the end of 2020: $5.5bn. One of the most high-profile fintech projects in the world.

- N26 (Germany): €1 billion in total customer funds. Apart from UK neobanks, an important European project that has announced its expansion into South America in 2020.

- SoFi (US), which describes itself as a ‘next-generation financial company’, takes an unconventional approach to lend and wealth management. Its StockBits product, for example, allows buyers to buy and sell fractions of 50 popular companies for just $1.

- Robinhood (US) offers a mobile app for trading stocks, ETFs, options, ADRs and cryptocurrencies for free. In September 2020, the startup raised $660 million in Series G funding. It raised US$660 million in Series G funding and was subsequently valued at US$11.7 billion.

- Klarna (Sweden) became Europe’s most expensive startup in 2020 with a $650 million investment, an installment shopping service that partners with global brands such as Adidas and H&M. Its partner network has 130,000 shops.

- Neon (Brazil). Its customers have access to unlimited, free interbank transfers and securities deposits that can be redeemed or used at any time. In June 2020, Neon bank announced a partnership with WhatsApp and integrated payments into the app

List of Best neo-bank

How to start a neo bank

Building a neobank seems difficult, and especially when you first start to learn about customer needs, it seems like an impossible mountain in front of you. But it’s not that difficult.

To start a neo-bank you need:

1. A banking license

There are two options: to get your own bank license or to rent one. The advantage of renting is that you can get started very quickly and reap the benefits in about six months. And you don’t have to pay that much. If you already have a banking license, you don’t need to do anything else.

2. A developer license for Apple and Google

You will need these to be able to develop your app.

3. Few helpers/mentors

You can build the neo bank yourself, but it is much quicker with helpers that can help you in developing the banking system, creating user interfaces and apps. Look for a mentor!

4. WordPress site or similar for your internet presence

There are many options to choose a cheap web hosting, but if you also want to give your NEO Bank a web frontend, it needs its own web hosting.

How does neobanks change the whole banking system?

Neobanks are declaring that they will not only change the old banking platform, but they will also change the way currencies are used around the world. These are beneficial ambitions for the future, but it is really difficult to imagine how it will be in the future. However, the strength of neobank is something we all acknowledge.

Building the initial foundation out of customer desires:

The ability to create a new ecosystem that inherits from the system is the basis of optimal development, creating better user experiences, and at a lower cost.

Remove barriers to money and money:

With customer-centric experiences, all old barriers and difficulties will be improved and completely removed, and transactions will be resolved in the fastest and easiest way.

Discount and fee reduction:

Most of the neobanks have reinforced the digital system, minimizing steps allowing customers to pay lower fees.

The new bank, new ideas:

What is controversial in neobank's claims is that the new neobank-creating bosses will bring new thinking to the industry. Although this claim is only on their basis, they use customer experience, artificial intelligence to create a new future for neobanks.

Troubleshooting neo-banking

Take a look at any of the websites listed above and it's clear that their target audience is the young generation, smart consumers.

But Eric Wilson, CEO of Xinja claims that 36% of their users are over 45 years old and 9% of users are over 65, and this user multiplier will change as they get full services and utilities.

Neo-banking has been around longer in Europe, where the population is older and everyone uses neobank. But Monzo, the top neobanks in the world, was founded in 2015 with only 1 million users while Revolut has access to 3 million.

The neobank adopts venture capital funding to accelerate its growth

Although the neo-banking are still facing many limited issues, they still have plenty of opportunities to expand and create their corridors worldwide. They are still able to replicate the same success that Europe did and put restrictions on other neobanks around the world.

Advantages of the neobanks

Since the neobanks are purely digital, technology and artificial intelligence, they open up a broad favorable opportunity for customers. And below are the advantages of neobank.

Quick account creation

Everyone knows and has spent the long wait when opening a new account at a mainstream bank. Surely no customer wants to experience it again. Especially when knowing the neobank with the maximum implementation procedures in just 3 minutes. Creating an account in digital banks is much simpler than you might think.

As learned above, neobank is a fully digital bank, thus eliminating the possibility of having a storefront. So users can create accounts without going anywhere. The neobank works entirely on a mobile device, making the process comfortable and the account will be ready in a very short amount of time.

Seamless and easy international money transfer payments

With traditional banks, there are always barriers to making payments and remittance money complicated and time-consuming. Customers who want to use international-related services must consider upgrading to a higher card or opening more debit/credit cards.

And neo-banking startups have overcome this weakness by allowing transactions and converting foreign currencies with the current exchange rate.

User-friendly interface

As mentioned, neobank is an application platform that cares about customer experience. Neobank always gives priority to creating smart and user-friendly handling interfaces, easy to understand and use. Neobank applications need to meet criteria such as fast, sharp and well-designed according to the needs of customers.

Service speed

Transactions of neobanks are almost immediately processed or regulated in a specific time period (international transactions). It provides you with a dashboard with complete information regarding activities and account balances. It also helps you manage your finances, spending through financial numbers, and helps you manage your crypto wallet better than ever.

Low transaction costs

One of the disadvantages of traditional banks is that high transaction costs often arise in the form of fees charged for services such as international money transfers, domestic transfers, other bank transfers, and bank statements. accounts, transaction notices, etc.

Low surcharge in neo-banking

Sometimes, customers pay a lot of money for fees, especially businesses when payment transactions happen every minute per second. Neo-banking eliminates this completely. It is technology-driven and provides a wide range of services to customers with just a few simple hands.

There is no existing infrastructure and maintenance for transaction branches and ATMs, resulting in additional savings in large fixed costs. Neobanks business model offer transactions free of charge in the app. Ignoring all the additional service fees, neobanks turn themselves into a great and promising alternative.

Value-added service

Neo-banking is not just about transfers and payments anymore. The neobank uses account information, customer data, templates, etc. with intelligence to propose necessary financial services according to the needs of customers.

Neobanks take advantage of customers' profits, introducing services based on demographics, behavior, and preferences to find more customers.

Advanced security features at neo-banking

Security is always the most important factor when it comes to digital transactions. A neo-banking application that implements 2FA (2-factor authorization), biometric verification, RBAC (Role-Based Access Control), encryption technology among other security measures to protect data customer data. The apps are built to ensure compliance with anti-money laundering laws, ensure customer privacy, and prevent malware attacks.

And the appearance of FinFan - Neobank with optimal solutions from "Cross Border Money Movement Platforms" to services of Bill payment, investment, loan. ..etc. Always make sure that you fully understand neobank digital banking to immediately use it instead of mainstream banks.

4 things to know about neobank

- The biggest benefit of neobank is not the deposit payment service, but the use of data available through the technology platform to provide customers with their financial visibility.

- By using a "user-centric" business, neobanks are attracting users to become a community and respond to their real needs.

- Many of the best neobanks have built important databases, applied artificial intelligence to see the potential of the future, and encouraged users to share their network with more people.

- The neobank adopts venture capital funding to accelerate its growth.

FinFan - Neobank in Vietnam

Hotline: +84 28 6685 331